How realistic is China’s five-year plan for robotics?

|

Listen to this article  |

The new five-year plan for the robotics industry is principally a good sign for China’s robotics industry. Whereas other parts of the Chinese technology sector have been hit by stricter regulatory measures in the past year, this plan highlights the ongoing political support for this field.

Whereas the Chinese government seems skeptical about much of the consumer internet, it wants to make China an industrial powerhouse, and robots are a part of this. This trend is also reflected by the fact that Chinese venture capital (VC) investments in robotics almost doubled in 2021 compared to 2020. VC funds in general raised 65% less capital during this period.

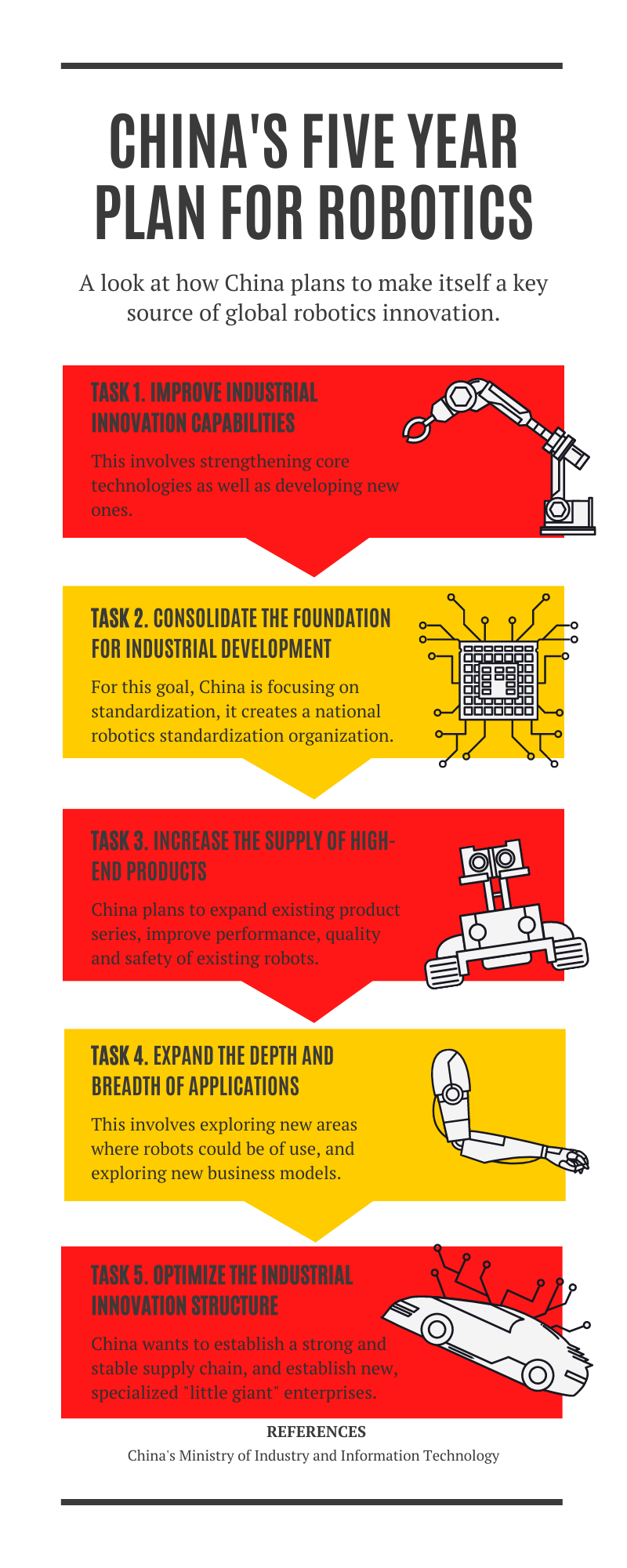

Regarding the goals and the question of how realistic they are, I expect a mixed outcome. We should not forget that this is not the first plan of this kind. The first five-year plan for the robotics industry was released in April 2016, about one year after the Made in China 2025 strategy.

Together with plenty of initiatives on provincial and city levels, the subsidies in the wake of Made in China 2025 turned out to be more of a curse than a blessing for the domestic robotics industry, however. Political connections often mattered more than technical capabilities for the distribution of subsidies. Huge overcapacities for the assembly of robot arms were built up, while the development of key components such as reducers, servos and controllers was neglected. Domestic robot companies were trapped in a vicious cycle of low technical capabilities and no margins at the low end of the value chain, leaving no space for investments in R&D.

Correspondingly, we didn’t see the market share of domestic robot makers grow for a long time, it has been around 30-35% over the last few years. The change was only in 2021, when we saw that local companies such as EFORT or ESTUN started winning tender offers against globally leading robot suppliers at renowned clients such as BYD or Foxconn. With extremely low prices, domestic makers of collaborative robots such as JAKA or Elite are also becoming more visible in low and mid end applications. The field of Kiva-like AGVs is dominated by local firms.

Speaking about core components, gains of local suppliers were also incremental until recently. Over the last year, we saw that firms such as Inovance (motion control) and Leaderdrive (harmonic gears) were growing stronger than the general market.

Have these recent successes been achieved due to the successful implementation of government planning? Some observers say they came more despite than because of the government policies. Domestic companies can only go into price wars when they have corresponding funding. As we have seen in China’s machine tool industry before, huge credit lines can lead to a lack of financial discipline, and prevent companies from becoming competitive in the long run.

Can China pick the right winners?

One of the goals of the new plan is to consolidate the industry and create larger entities. However, it is not entirely clear if the government is good at picking winners.

An example of success is HIKROBOT, the logistics robot branch of HIKVISION, China‘s leading state-owned supplier of video surveillance equipment. Together with Huawei, the companies are working on innovative autonomous navigation solutions, which can work without expensive LiDARs.

Cheaper mobile robots might be a game changer, indeed. The achille’s heel of both these companies is their proximity to the Chinese state and that they are on U.S. entity lists. New technologies such as autonomous navigation require substantial computing power, and no mainland Chinese company is close to being able to produce processors powerful enough to complete these tasks.

An example where close government ties do not necessarily translate into success in the marketplace is Siasun, one of China‘s oldest and largest state-owned robot manufacturers. The company had the lowest sales growth among the top 20 robot vendors in China during the last two years.

Takeaways

To conclude, even if many of the goals in this plan are not entirely new and might not be reached in time, both robotics companies and policy makers outside of China need to take the challenge from China’s robotics industry seriously.

Recent developments make me more optimistic about the capabilities of local companies than five years ago. China has increased its number of robotics scientists, many of them educated abroad. The country‘s large industrial base provides plenty of sales potential. In fields such as battery making or photovoltaics, China is so advanced that production knowhow from there is now transferred to other countries. Subsidies and fierce competition in China are bringing down prices, which will pave the way for new robotics applications. Even we expect the economy to cool down further in 2022, promising robotics companies will continue to receive support.

On the other hand, state-funded Chinese robotics companies are eyeing the US and the EU, hoping to charge higher prices there than in their hyper-competitive home market. Western robotics companies need to be prepared for that. Policy makers must find ways to sustain a healthy development of future industries against competitors, which are enjoying unfair state aid.

Last, but not least: policy makers in the West need to ask themselves what they can do to create a better environment for technology companies on their side. Speaking as a German citizen, our government should be reminded that the fight against climate change is important, but that there are also other pressing issues. Too many resources are being spent for unproductive activities, these days. When were the last attempts to unleash more creative, entrepreneurial power and encourage risk takers in the EU?

Credit: Source link

Comments are closed.