Australian sportstech is now a $4.25 billion industry

Local sportstech is now worth as much as the fintech startup sector, with more than 750 companies involved, according to new analysis from the Australian Sports Technologies Network (ASTN).

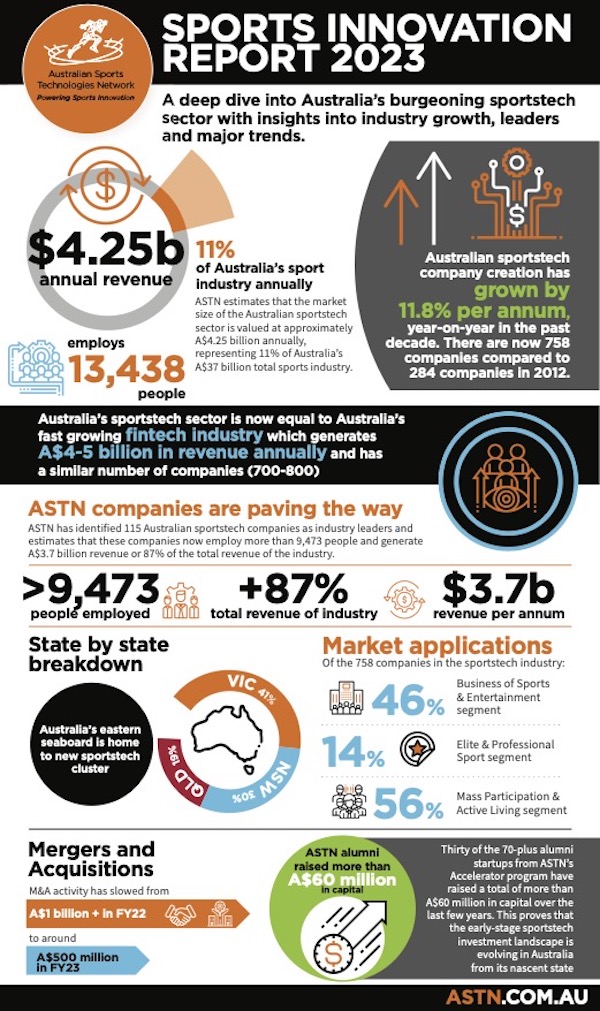

Releasing its second annual Sports Innovation Report for 2023, ASTN put the value of sportstech at $4.25 billion as the sector begins to ramp up for the 2032 Brisbane Olympics. It now represents 11% of the sports industry overall.

ASTN chair Dr Martin Schlegel said they uncovered 758 companies in the local sportstech ecosystem, now employing 13,438 people. That figure means the sector has grown by 11.8% per annum in the decade since the peak body for sports technology and innovation launched in 2012 with 284 companies.

“Rapid growth in sportstech is reshaping the sports industry as we know it, and unlocking new revenue streams,” Dr Schegel said.

“The second edition of the ASTN Sports Innovation Report takes a deeper dive into the emerging sector – to help inform industry leaders, and provide new growth opportunities for sportstech startups.”

ASTN CEO Dr Martin Schlegel

The report identifies 115 companies as industry leaders, including brands such as 2XU, SWEAT, VULY and PTP. Those companies generate around 87% of the total revenue of the industry.

“Australia’s sportstech sector has proved it has now moved out of its nascent stage as it goes head-to-head with Australia’s booming fintech sector. Australia continues to prove that it’s one of the world’s leaders and long-term pioneers in sports technology and innovation,” Dr Schlegel said

” The sector has exceeded all expectations in this year’s report as the sector surpasses $4 billion in revenue.”

The rise of Australian sportstech aligns with its exponential rise globally. It’s estimated to be worth US$22.9 billion (A$34.65bn) in 2022, and expected to grow by 13.8% per annum to US$41.8+ billion (A$63.2bn) by 2027.

Going for gold

Meanwhile, Dr Schlegel believes the Brisbane 2032 Olympics and Paralympic Games will provide new opportunities for the sector to develop a new wave of technology solutions.

“We are building one of the world’s most advanced and integrated sportstech ecosystems in the lead up to several major events in Australia’s sporting calendar over the next decade,” he said.

“We can expect to see new technologies from AI, big data analytics to mobile, non-invasive wearable sensors and smart materials being deployed across the sportstech market verticals. As a result, new companies will be formed providing opportunity for further growth of the sector.”

10 trends

The report identifies 10 major themes that provide strategic opportunities for the industry, from ESG to active Living, fitness & wellness, and smart apparel, which have accelerated digital transformation across leagues, teams and federations.

Many of the emerging trends, such as artificial intelligence, emerging sports, and women in sportstech form part of ASTN’s five-year strategy.

Dr Schlegel said startups, companies, founders, government and the wider sports industry must recognise and embrace these themes, looking at how they impact current activities, how they need to evolve and adapt, and what opportunities they present.

“To continue the sectors momentum, Australia’s sportstech firms need to stay abreast of global trends and take advantage of these opportunities to reap the rewards over the next decade,” he said.

“There’s still an enormous amount of untapped opportunity in the local sportstech ecosystem. Australia’s sportstech sector is manifesting its position as an ideal incubation and validation market with our global counterparts acknowledging the capability and quality of sportstech solutions derived here.”

Key findings

The key report findings are:

- Sportstech employment by state: Of the 13,438 people employed in sportstech, ASTN estimates that nearly half (47%) of sportstech jobs are based in Victoria, followed by NSW (27%) and QLD (18%).

- Sportstech location: The majority of sportstech companies are based in Victoria (41%), New South Wales (31%) and Queensland (19%) – with a concentration of activity in the three key metro areas including Melbourne, Sydney and South East Queensland.

- M&A activity has slowed: There has been a decline in mergers and acquisition (M&A) and capital raising activities in FY23 compared to FY22 – due to significant tightening of access to investment capital, driven by rising interest rates and inflationary pressures. M&A activity has slowed to around A$500 million in FY23, compared to over A$1 billion in FY22.

- ASTN companies are paving the way: Sportstech companies mentored by ASTN programs now employ 270 people, and thirty of the 70-plus alumni startups from ASTN’s Accelerator program have raised a total of more than A$60 million in capital over the last few years.

- Mass Participation & Active Living market dominatesM: ASTN has found the majority of companies (56%) provide their products and solutions to the Mass Participation & Active Living market, followed by Business of Sport & Entertainment market (46%) and Professional & Elite Sport (14%).

- ICT continues to be the largest technology category: The majority of companies develop their solutions using Information and Communication Technologies (ICT) (66%), followed by Advanced Materials (23%) to build their products.

- Emerging sportstech trends present new opportunities: ASTN’s top 10 themes are:

- 1. Artificial Intelligence (AI),

- 2. Active Living, Fitness and Wellness,

- 3. Web 3.0, Metaverse, Gaming and Blockchain,

- 4. Virtual Sports of Tomorrow

- 5. Smart Apparel, Equipment and Wearables

- 6. ESG,

- 7. Sports Digital Ethics, Privacy and Security

- 8. Women in Sportstech,

- 9. Investment and Venture Capital,

- 10. Global Trade and Business Matching.

The full Sports Innovation Report 2023 can be downloaded here.

The 2023 ASTN Sports Innovation Report highlights

Credit: Source link

Comments are closed.