Review: Venture capital is a victim of own success

A U.S. $100 dollar bill is seen December 17, 2009.

Register now for FREE unlimited access to Reuters.com

Register

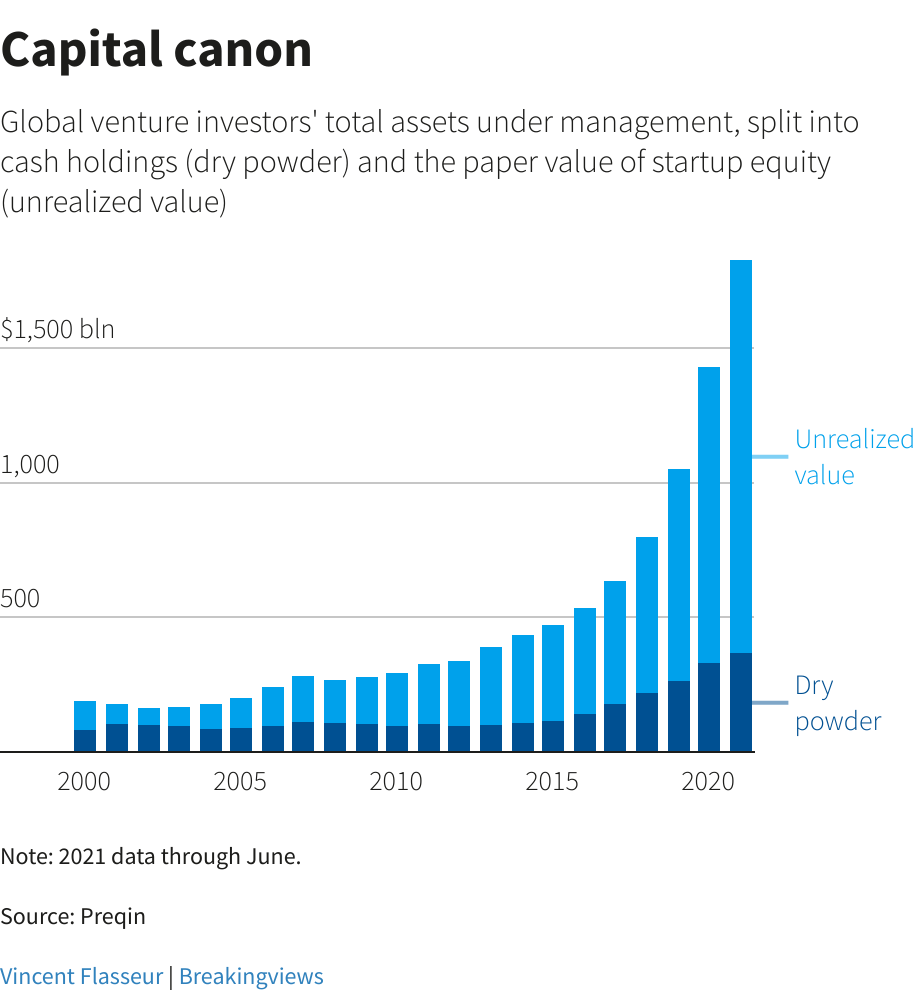

LONDON, Jan 21 (Reuters Breakingviews) – What’s good for venture capital isn’t necessarily good for venture capitalists. That’s one message from “The Power Law: Venture Capital and the Art of Disruption”, Sebastian Mallaby’s absorbing new history of startup investing. Successful early technology backers invited imitators, making capital into a commodity and empowering cocksure founders. Even as the $1.8 trillion industry breaks fundraising and dealmaking records, its influence over companies may have peaked.

Mallaby traces venture investing’s origins to the late 1950s, when financier Arthur Rock helped eight frustrated engineers splinter off from their capricious boss to found Fairchild Semiconductor. The investment terms would make modern VCs drool: in return for $1.4 million, the backers retained an option to buy the whole company for $3 million. By 1959, the transistor designer’s net income was $2 million, meaning the funder could take it over at a multiple of just 1.5 times earnings. At the time, IBM (IBM.N) shares were trading at a price-earnings ratio of 50.

Unsurprisingly, the model caught on. But startup funding remained scarce enough that VCs had the upper hand in negotiations with entrepreneurs. That only seemed fair. After all, while mainstream investors like Warren Buffett advocated buying shares at a discount to a company’s book value, the VCs were offering cash to unprofitable ventures that had no tangible assets – “finance without finance”, as Mallaby puts it. Most of those bets would fail. But one home run like Fairchild or rival chipmaker Intel would more than compensate for the losses.

Register now for FREE unlimited access to Reuters.com

Register

Hence pioneers like Sequoia Capital’s Don Valentine and Tom Perkins of Kleiner Perkins at times wielded more influence than the entrepreneurs they backed. Valentine in 1976 steamrollered the founder of Atari into selling the computer games group, tripling Sequoia’s money and scoring a vital early win for the fledgling fund.

Perkins, who struck up a partnership with one of the original Fairchild tearaways, was even more hands-on. At Genentech he pushed management to contract out research rather than doing everything in-house. Perkins would roar up to the biotechnology group’s office in his Ferrari to dispatch orders and announce product deadlines. “Don’t come back until you’ve got insulin done”, he instructed one researcher after summoning him to dinner at his hilltop mansion. In 1980, Genentech went public and Kleiner Perkins made its money back 200 times over.

Mallaby presents these examples as evidence for one of his core arguments: venture investing is mostly about skill rather than luck. That’s contentious. After all, the Genentech scientist may have “got insulin done” regardless of Perkins’ intervention. Atari might have been worth more if it waited longer before selling out. These days, investors in startups often admit that their best investments come from being in the right place at the right time, while pointing to evidence that suggests inexperienced founders benefit from their guidance.

Mallaby extolls the ways Sequoia, Accel, Benchmark and others make their own luck by cultivating vast networks and hiring partners with deep technical expertise. He spends less time on the graveyard of firms that tried the same approach but didn’t uncover a lottery-winning startup like Airbnb (ABNB.O) or Stripe. One academic study finds that success begets success, suggesting established VC firms get better access to attractive deals, boosting their odds of landing a home-run. Does that mean storied VCs are free riding on the hard work and inventiveness of entrepreneurs?

By the 1990s and early 2000s, founders were asking themselves similar questions. Paul Graham, who founded e-commerce facilitator Viaweb and would go on to establish investor-cum-boot camp Y Combinator, published his Unified Theory of VC Suckage. Meanwhile the capital that flooded into Silicon Valley chasing internet-based riches tilted the balance of power. Sergey Brin and Larry Page of Google initially raised money from wealthy technologists rather than VCs. In 1999, they dictated terms to Sequoia and Kleiner Perkins, offering them each 12.5% of the search engine in return for $12 million. “I have never paid more money for so little a stake in a startup”, said John Doerr of Kleiner Perkins.

It was just one example of an inexorable power shift. In the 1960s, Fairchild backer Rock expected 45% of any startup he financed and would sometimes chair the board. The standard VC holding dropped to one-third in the 1970s and 1980s. Google’s Brin and Page gave up one-quarter of the company in 1999, while Accel got just one-eighth of Facebook in 2005, after founder Mark Zuckerberg insulted Sequoia by arriving late to a meeting wearing pyjama bottoms. Single-digit percentages are now common. Late-stage megafunds like Tiger Global write enormous cheques without expecting a seat on the board.

The wall of money has turned VCs from activist investors into cheerleaders. One of Uber Technologies’ (UBER.N) early backers shaved the ride-hailing company’s logo into his hair. Such obsequiousness may help to land deals but also empowers cocksure entrepreneurs who can use super-voting shares to entrench themselves. Benchmark’s Bill Gurley just about managed to oust Uber’s untameable founder Travis Kalanick. WeWork’s Adam Neumann is the ultimate cautionary tale. In short, Mallaby’s history shows that the cult of the founder is mostly a consequence of capital becoming a commodity.

The continued influx of venture money would therefore suggest that founder power will only increase further. Perhaps that’s no bad thing if entrepreneurs were the ones creating value all along. But if Mallaby is right, and investors’ interventions were integral to building Silicon Valley’s great companies, their waning influence suggests trouble ahead.

Follow @liamwardproud on Twitter

(The author is a Reuters Breakingviews columnist. The opinions expressed are his own.)

CONTEXT NEWS

– “The Power Law: Venture Capital and the Art of Disruption” by Sebastian Mallaby will be published by Allen Lane, an imprint of Penguin Books, on Jan. 25.

Register now for FREE unlimited access to Reuters.com

Register

Editing by Peter Thal Larsen and Karen Kwok. Graphic by Vincent Flasseur.

Reuters Breakingviews is the world’s leading source of agenda-setting financial insight. As the Reuters brand for financial commentary, we dissect the big business and economic stories as they break around the world every day. A global team of about 30 correspondents in New York, London, Hong Kong and other major cities provides expert analysis in real time.

Sign up for a free trial of our full service at https://www.breakingviews.com/trial and follow us on Twitter @Breakingviews and at www.breakingviews.com. All opinions expressed are those of the authors.

Credit: Source link

Comments are closed.