Space Capital sees upside to 2022 decline in space investment

SAN FRANCISCO – Last year was rough for many space startups.

Overall investment dropped 58 percent from its $47.4 billion peak in 2021 to $20.1 billion in 2022. Still, Chad Anderson, Space Capital managing partner, thinks the downturn will make the sector more resilient.

“We see the shift away from momentum investing and back to a focus on fundamentals as a net positive for the space economy, since it will reward quality companies and discipline those that have weaker fundamentals and are struggling to execute,” Anderson said by email.

Over the longer term, the shift in investment philosophy will help streamline the sector, “thereby reducing competition and allowing strong companies to thrive,” Anderson said. “This will make the space economy stronger, more efficient and more resilient.”

Space Capital, a New York-based venture capital firm, published its Space Investment Quarterly Jan. 19 for the fourth quarter of 2022. The report notes that early-stage startups fared better than later-stage and growth companies.

One exception was SpaceX, which raised $2 billion in 2022, or 32 percent of the total 2022 private investment in space infrastructure.

SpaceX was also in the minority because it raised capital in both 2021 and 2022. Only 38 percent of the space infrastructure companies that raised capital in 2021 sought additional funding in 2022.

SpaceX is such an outlier that it’s sometimes tempting to consider the annual investment picture without the launch giant.

Without SpaceX, though, “you wouldn’t really have a viable infrastructure layer to speak of,” Anderson said. “SpaceX is largely responsible for creating the space economy as we know it today and it clearly dominates the launch industry. We can’t talk about infrastructure without considering SpaceX and this is not going to change anytime soon. In fact, it’s only going to become more integral to the space economy once Starship comes online. Starship promises to revolutionize launch, but it will also create massive opportunity – and disruption – across many other industries including stations, lunar, on-orbit manufacturing, and debris clean-up.”

Over the last decade investors bet $272.3 billion on 1,791 space companies. The totals include hardware and software firms that work with space data as well as companies firms that use space data from space assets in their products or services.

Looking ahead, Space Capital expects 2023 to be a difficult year for startups as investors remain selective.

“Many investors, who view space as primarily infrastructure, view space as a higher risk asset class,” Anderson said. “So, they will be much more selective in how they invest.”

That trend will force pre-revenue companies and firms with questionable business models to “reckon with market forces, but there is a general risk here of throwing out the baby with the bathwater,” Anderson said. “It’s important for investors to understand that quality companies with strong fundamentals, particularly those with government, defense and intelligence use-cases, like satellite communications and Earth imaging, have strong growth prospects throughout 2023 and beyond.”

Venture capital firms have more than $200 billion in pent-up capital, but it will take several years to deploy the money since massive rounds remain rare, Anderson added.

In 2023, government spending will be increasingly important to the space economy, according to the Space Capital report.

“It is our view that space companies with government and defense applications will be best positioned to weather the tougher economic climate,” Anderson said. “National Security Space is now one of the fastest growing areas of the Department of Defense budget.

The $26.3 billion 2023 budget for the U.S. Space Force tops NASA’s $25.4 billion budget.

“Strategic competition with China will be a significant driver of US government spending in multiple areas of the space economy, from launch and satellites to low-Earth orbit logistics,” Anderson said. “However, one area where it will have an outsized influence is in the lunar industry. These commercial operations are high-cost, high-risk and with a long-term path to profitability, so without government support they would not be viable.”

The Artemis program is benefiting from the U.S. government’s determination to beat China to areas of the moon with resources like water-ice deposits.

“For this reason, while lunar might otherwise be a riskier category with the potential for wavering government support, we see this as a promising nascent industry with reliable growth prospects this year and the foreseeable future, due to the China factor,” Andreson added.

Space Capital is an investor in Astrobotic and Lunar Outpost, two firms preparing to conduct robotic lunar missions in 2023.

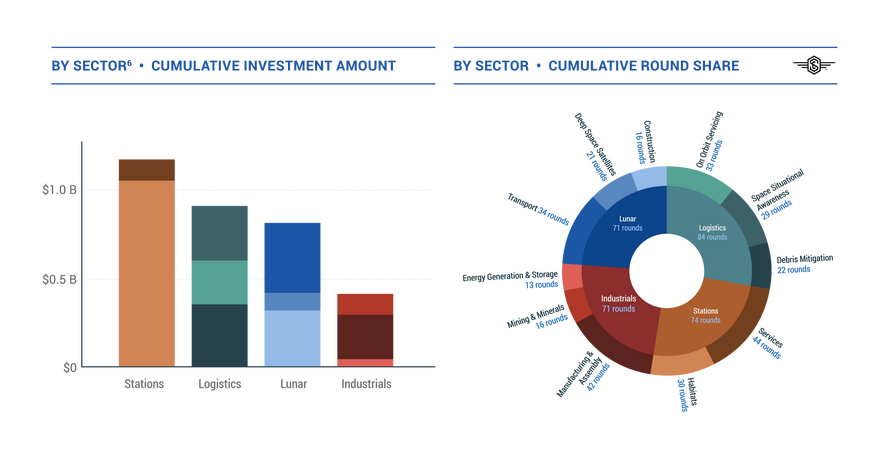

Investment in emerging industries dipped 63 percent in 2022 compared with 2021. Still, 2021 was a record for private investment in commercial space stations, lunar transport, debris mitigation, on-orbit servicing, in-space manufacturing and mining, and 2022 was the second best year.

“We broke out the Emerging Industries for the first time in our Space Investment Quarterly this year, which shows that $3.3 billion has been invested over the past decade, with nearly half of that total invested in 2021 alone,” Anderson said. “This record level of investment was driven by venture capital firms, many of whom were investing in the category for the first time. Unfortunately, a lot of bad deals got done in the peak of market mania, and those companies are now struggling in this market environment. Overall, we expect the macro market environment will continue to disproportionately affect funding for these capital-intensive companies, operating in limited new markets, for the foreseeable future.”

Credit: Source link

Comments are closed.