The role of venture capital and governments in clean energy

The role of venture capital and governments in clean energy: Lessons from the first cleantech bubble

In its 2022 special report, the Intergovernmental Panel on Climate Change declared that to limit global warming to 1.5°C above pre-industrial levels, the world needs to invest $2.3 trillion every year in low-carbon electricity technologies alone. However, Bloomberg’s New Energy Finance estimates that only $755 billion was invested globally in energy transition sectors in 2021. This funding gap is particularly acute in the early stages of innovative clean technologies (Polzin and Sanders 2020). These clean technologies, known as cleantech, aim to provide clean energy and sustainable products.

In this context, the recent boom in ‘cleantech’ venture capital (VC), a type of funding for young, high-growth companies, is encouraging. This surge in ‘green’ VC funding has two primary sources. First, the VC sector as a whole has been experiencing a boom. Second, investors – spurred by the climate crisis and growing public support for innovative solutions – are increasingly keen to invest in new clean technologies. In October 2021, Larry Fink, the CEO of the world’s largest asset manager, argued that the next 1,000 start-ups worth more than $1 billion would be in clean technologies (Clifford 2021).

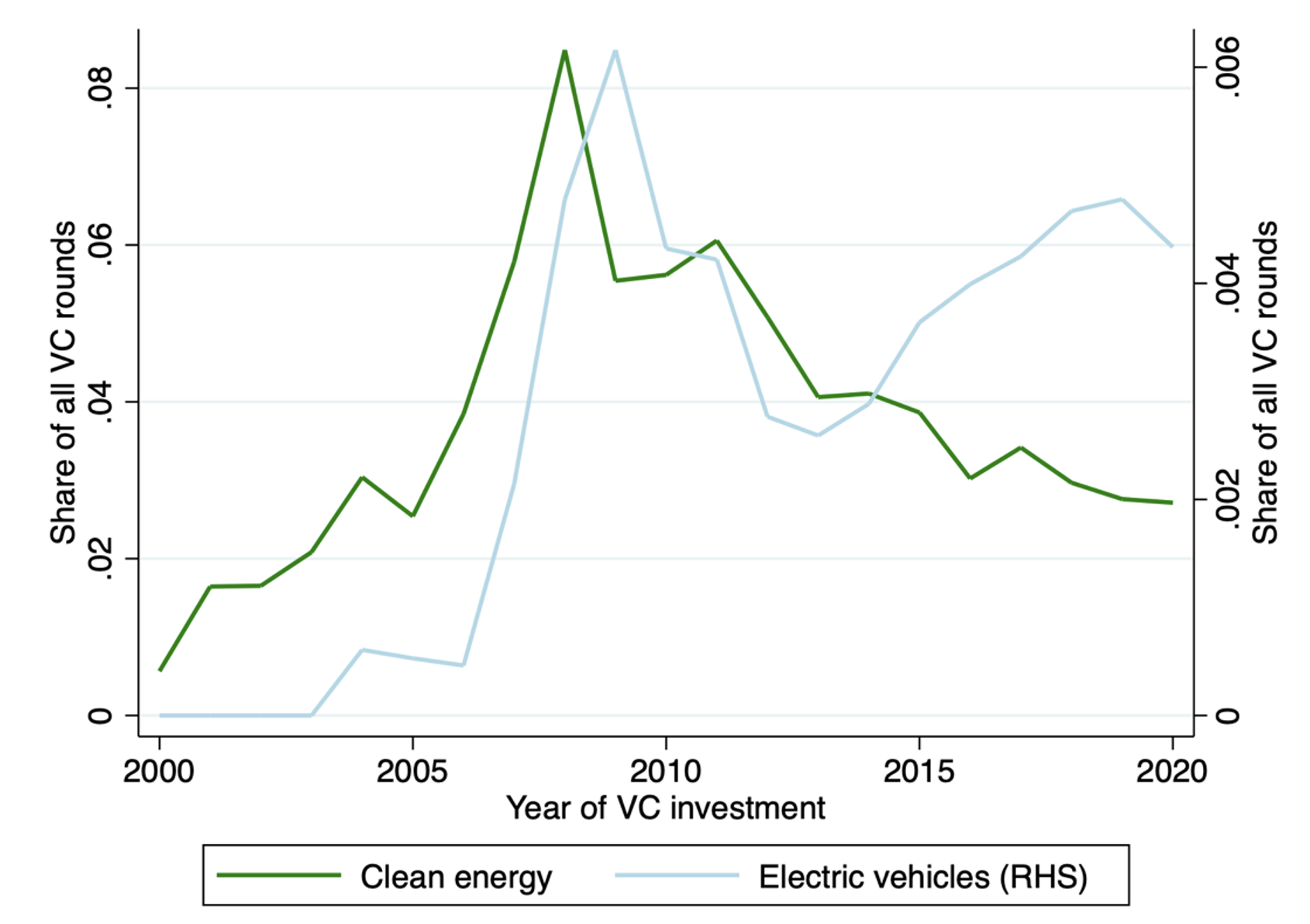

One might wonder whether this optimism is warranted. In fact, this new wave of investments and interest in cleantech is reminiscent of the boom-and-bust cycle that happened from 2005 to 2013 (see Figure 1). At that time, the rapidly growing interest in clean energy from policymakers resulted in a similar surge in green investments. From 2005 to 2008, the share of VC funding going to clean energy technologies more than tripled. However, clean energy start-ups proved to be an unprofitable experiment. Less than half of the over $25 billion provided to cleantech start-ups from 2006 to 2011 was returned to investors (Gaddy et al. 2017). As a result, the cleantech boom went bust as VC funding dried up.

In our recent paper (van den Heuvel and Popp 2022), we use Crunchbase data on 150,000 US start-ups active between January 2000 and May 2021 to draw novel insights from the initial failure of cleantech VC. A better understanding of exactly why early venture capital efforts failed can help assess the possibility of success for this second, less energy-focused, wave of green venture capital investment and inform policies aimed at supporting new clean technologies.

Figure 1 The cleantech boom and bust

Notes: This figure shows the share of all VC rounds (Series A to Series J) going to clean energy (LHS) and electric vehicles (RHS).

The reasons behind the failure of venture capital in cleantech

Studies addressing the cleantech boom and bust offer multiple explanations for VCs’ poor performance in cleantech and particularly in clean energy start-ups (Hargadon and Kenney 2012, Nanda et al. 2015). First, developing new clean energy technologies is capital-intensive and slow to scale, resulting in unattractively long payback periods (Migendt et al. 2017). Second, many clean energy start-ups operate in very competitive markets with thin margins, making it difficult to earn the outsized returns that VCs seek. Many clean energy start-ups offer a product – renewable energy – that is hard to differentiate from the energy produced by non-renewable sources. Finally, while investing in any start-up is inherently risky, cleantech start-ups expose investors to additional risks – ones that arise from producing a commodity that is influenced by volatile international markets or those associated with demand being dependent on public policies that can prove unstable (Noailly et al. 2022).

Our paper examines whether these explanations are supported by recent data. Comparing the performance of less capital-intensive digital energy start-ups (e.g. smart thermostats) to other firms suggests that the high capital intensity and long development timeframe of clean energy start-ups is not the main factor behind the lack of success of VCs. Indeed, while less capital-intensive digital energy start-ups did fare better in the early stages of the cleantech bust, these start-ups eventually also experienced a fall in their profitability and ability to secure VC funding (see Figure 2). At the same time, biotech and electric vehicles have been able to attract investors in recent years despite being capital-intensive.

Figure 2 Venture capital’s willingness to fund energy digital start-ups has also fallen

Notes: This figure displays the share of all start-ups that manage to secure Series A funding, based on the year they were launched, by industry. Values are not displayed for energy digital start-ups launched before 2005 because of the low data availability (i.e. only three to eight start-ups were funded each year).

Instead, we argue that weak demand for clean energy technology, resulting from a failed attempt at a nationwide US climate policy, is the main reason behind the failure of VC in clean energy. After years of growing policy support, VC investments in cleantech peaked just as environmental regulations suffered setbacks with the failure of the cap-and-trade bill in the US Congress and the disappointing Copenhagen Climate Change Conference (COP15) in 2019. We use an exogenous negative shock to study the effect of changes in expectations of future climate policy support: the unexpected loss of the Democrats’ filibuster-proof majority in the Senate in January 2010.

We find that expectations of weaker demand significantly impacted VCs’ willingness to fund clean energy start-ups, as it made marginal investments less attractive. The fall in expectations of policy support led VCs to invest in fewer – but higher quality – cleantech start-ups that performed better than the start-ups funded before the shock under more optimistic policy expectations.

We also confirm a second reason for the failure of cleantech VC. We show that clean energy start-ups are significantly less likely to become home run successes than information and communications technology (ICT) or biotech ventures. The lack of network effects, the lesser reliance on patents, and lower product differentiation make it harder to keep competitors at bay and earn high margins in clean energy. This prevents the formation of ‘winner takes all’ markets that make ICT or biotech start-ups so attractive.

The future of clean technology innovation and the government’s role

The importance of strong demand can help us understand the second boom in cleantech VC and provide insights into which investments are more likely to succeed. First, government policies are becoming more supportive than they were in 2009 (Popp et al. 2020). In the EU, the Fit for 55 plan aims to reduce greenhouse gas emissions by 55% (relative to 1990 levels) by 2030. While national climate policy remains unattainable in the US, many states have ambitious clean energy goals, such as California’s plan to rely on zero-emission energy sources by 2045. This increasingly supportive policy environment is boosting demand for all clean technologies.

However, VC investments in clean energy will likely continue lagging behind other cleantech sectors like electric vehicles (EVs), as seen in Figure 1. Indeed, VCs have learned to focus on cleantech sectors with existing high demand, where using the ‘clean’ technology requires little sacrifice (The Economist 2021). Some sectors, such as electric vehicles or sustainable food (e.g. plant-based meats), have few barriers to mass adoption and can differentiate their products, which fuels demand and improves profitability. The ability of firms like Tesla to manage their brand and bolster demand for their particular electric vehicles allows them to generate markups unattainable in the more competitive renewable energy industry.

These attractive features have translated into several recent home run successes in cleantech. Tesla returned 20 times the invested capital during its initial public offering (IPO) in 2010, but its valuation has since multiplied several hundredfold. This has whetted the appetite for investment in the area. Nikola Motor Company, a producer of electric trucks, returned 125 times the paid-in capital to its Series A investors when it went public in 2020. A similar pattern has been visible in sustainable food. Impossible Foods, a maker of plant-based meats, is now valued at $7 billion and could go public in 2022, returning 82 times to its early-stage investors.

These companies have proven that some cleantech sectors can produce outsized returns, fuelling this new cleantech boom. As a result, the second boom in VC may result in better outcomes than its predecessor. However, clean energy start-ups will likely continue to struggle to attract VC funding. As more innovation in clean energy is needed to address climate change, governments should do more.

With that in mind, we also study the performance of public investments in cleantech start-ups (Bai et al. 2021). We find that public investors have not fared worse than their private sector counterparts. However, since VC investments in clean energy as a whole perform much worse than in other sectors, simply matching private sector performance in the clean energy sector is not enough. Without a more robust demand for clean technologies, neither public nor private investors are likely to be consistently successful when funding clean energy start-ups. By implementing persistent demand-side policies (e.g. a meaningful carbon tax), governments would improve the expected performance of early-stage investors, helping reduce the funding gaps in clean technologies. Only then should governments use targeted public investments to fund the cleantech start-ups that will still struggle to attract private sector investments, notably because they have a limited potential for outsized returns.

Authors’ note: The views and opinions expressed in this column are strictly those of the authors, and do not necessarily represent the views or opinions of The Brattle Group (“Brattle”) or any of its other employees or clients. Readers of this column should seek independent expert advice regarding any information in this article and any conclusions that could be drawn from this report. The article itself in no way offers to serve as a substitute for such independent expert advice.

References

Bai, J, S Bernstein, A Dev and J Lerner (2021), “The government as an (effective) venture capitalist”, VoxEU.org, 14 May.

Clifford, C (2021), “Blackrock CEO Larry Fink: The next 1,000 billion-dollar startups will be in climate tech”, CNBC, 25 October.

Gaddy, B E, V Sivaram, T B Jones and L Wayman (2017), “Venture Capital and Cleantech: The wrong model for energy innovation”, Energy Policy 102: 385–395.

Hargadon, A B and M Kenney (2012), “Misguided policy? Following venture capital into clean technology”, California Management Review 54(2): 118–139.

Lerner, J and R Nanda (2020), “Venture Capital’s Role in Financing Innovation: What We Know and How Much We Still Need to Learn”, Journal of Economic Perspectives 34(3): 237–261.

Migendt, M, F Polzin, F Schock, F A Täube and P von Flotow (2017), “Beyond venture capital: An exploratory study of the finance-innovation-policy nexus in cleantech”, Industrial and Corporate Change 26(6): 973–996.

Nanda, R, K Younge and L Fleming (2015), “Innovation and Entrepreneurship in Renewable Energy”, in The Changing Frontier (Issue July, pp. 199–232), University of Chicago Press.

Noailly, J, L Nowzohour and M van den Heuvel (2022), “Does Environmental Policy Uncertainty Hinder Investments Towards a Low-Carbon Economy?”, CIES Research Paper 74.

Polzin, F and M Sanders (2020), “How to finance the transition to low-carbon energy in Europe?”, Energy Policy 147, 111863.

Popp, D, F Vona and J Noailly (2020), “Green stimulus, jobs and the post-pandemic green recovery”, VoxEU.org, 4 July.

The Economist (2021), “Billions are pouring into the business of decarbonization”, 19 August.

van den Heuvel, M and D Popp (2022), “The Role of Venture Capital and Governments in Clean Energy: Lessons from the First Cleantech Bubble”, NBER Working Paper Series.

Credit: Source link

Comments are closed.