The startup and venture markets are coming back to square one • TechCrunch

What goes up must come down” is a cliche that is also a bastardization of Newton’s third law. It’s also a good reminder that when it looks like the business market has changed fundamentally, we’re often really just seeing a temporary aberration.

This idiom rings true when we consider the cycle of tech valuations (up and then down), venture capital (up and then down), and the pace at which new unicorns are being minted (also up and then down). These three trends are linked, obviously, but what gave us pause recently was the realization that we haven’t merely seen declines in recent quarters: instead, there’s been a whole-cloth return to pre-COVID norms.

The Exchange explores startups, markets and money.

Read it every morning on TechCrunch+ or get The Exchange newsletter every Saturday.

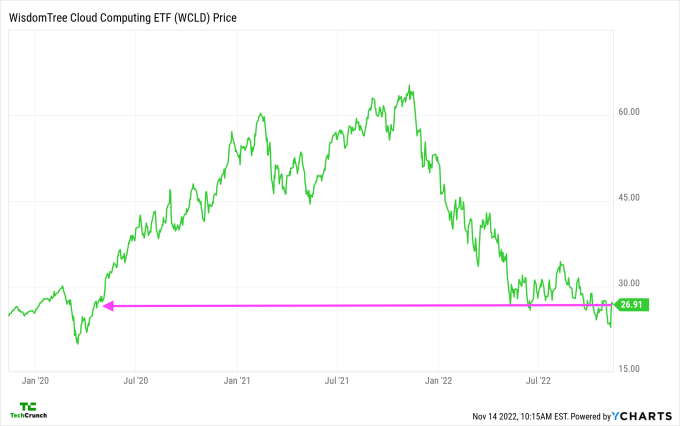

Take tech valuations, for example: It struck us this morning while drafting the weekly kick-off Equity episode that the value of tech stocks — measured through our favorite software-company tracking index — is today trading around the value it had in early 2020, just before and after the massive COVID-induced sell-off hit American stocks:

Please excuse our annotation method — it’s Monday.

It’s clear that the 2020-2021 boom in software valuations was more of an anomaly than a new-normal. Besides, the fact that the companies in the index grew over the last few years but are worth less today implies that they might have been overvalued even pre-COVID. If today’s prices hold up, they will indict not only the excess of the recent past, but the overvaluations of the 2010s as well.

Credit: Source link

Comments are closed.