Too many startups, not enough chairs when the music stops

Cheap money and the fear of missing out on outsized returns drove VCs to deploy capital into whatever companies they could. This dynamic dissolved as inflation elicited higher interest rates by the Federal Reserve, which shrank public market valuations and dampened growth expectations across the economy.

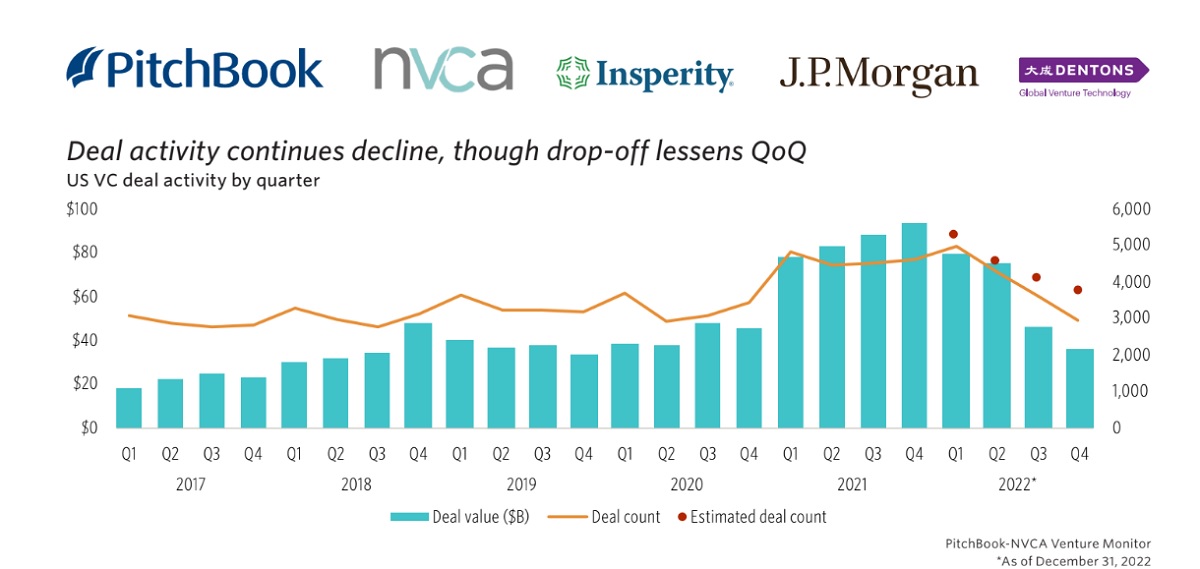

Due to the opaque nature of private markets, though, the current environment has created a puzzling disconnect. We have not seen a major pullback in US startup valuations, deal activity, or dry powder. And yet sentiment in the venture market has turned notably sour.

To clarify what is happening, we present a new metric that quantifies the supply and demand of capital between startups and VCs.

Startups in 2021 expanded operations and increased their demand for capital. This means that while deal activity has not slowed drastically, it does not support current capital demands.

We estimate that unfilled demand by US startups reached $42.8 billion in Q4 2022. Put another way, startups demanded more than twice as much capital as VCs supplied.

This bid-ask imbalance has been an issue across stages, but nowhere is it more overextended than at the later stage, with capital demand outpacing supply by 148.5%. That figure is 50.5% and 67.1% for the early and venture growth stages, respectively.

Startups are feeling this gap as deal terms shift in favor of investors, as evidenced by PitchBook’s VC Dealmaking Indicator (updated monthly). This imbalance will right itself in the long term, but there is misery ahead for startups searching for a chair now that the music has stopped.

To find out more, download our analyst note: When Dry Powder Stays Dry

Please reach out with any questions or feedback.

Credit: Source link

Comments are closed.