Venture capital business key to Valley National’s deal for Bank Leumi

Valley National Bancorp’s agreement to buy Bank Leumi USA — its biggest deal to date — would give it a strong opening in venture-capital banking.

One appeal of VC banking is the clients do not expect high interest rates on their deposits. Bank Leumi USA’s overall cost on its more than $7 billion in deposits is about 10 basis points, compared with Valley’s 22 basis points. The VC and tech business line contributes nearly $2 billion of deposits that carry just 3 basis points of cost.

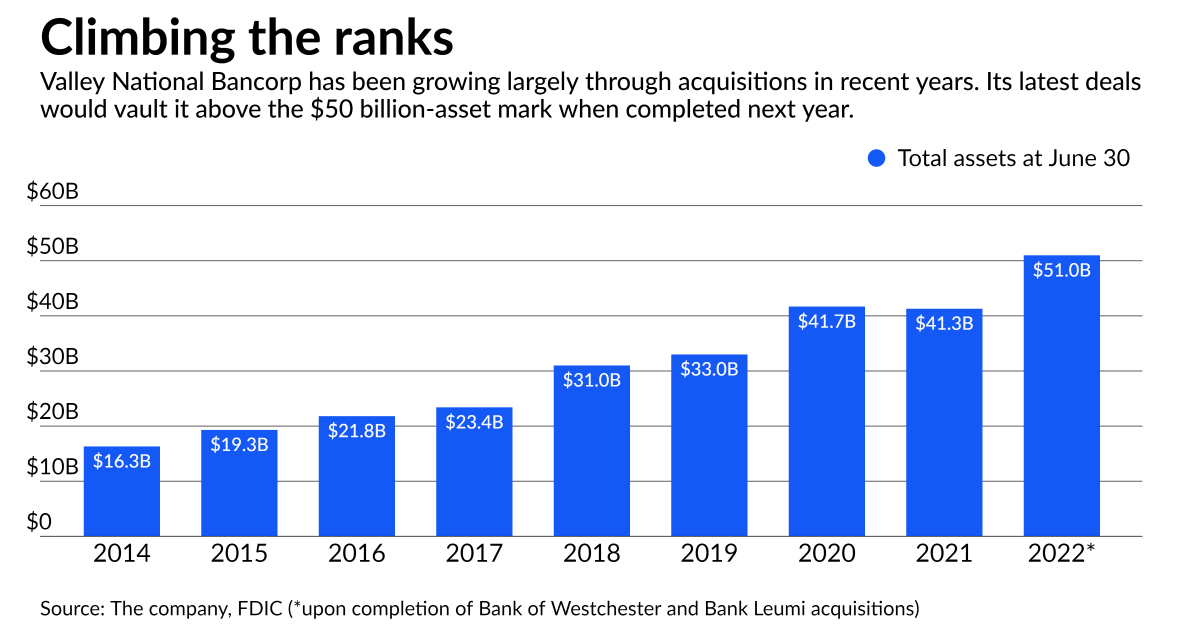

The $41.3 billion-asset Valley National in New York would pay about $1.15 billion in cash and stock for Bank Leumi USA, a unit of Bank Leumi Le-Israel Corp. Though the deal was not driven by geography, it adds offices in Chicago and Los Angeles — as well as Silicon Valley and Israel, two hot spots of tech innovation.

“This will be a new business line to Valley, but it’s one that we have considered building on our own in the past,” Ira Robbins, chairman and CEO of Valley, said in a conference call with analysts. “By acquiring this capability through Leumi, we will significantly accelerate this timeline to relevancy in this area.”

Bank Leumi USA has operated the VC and tech business line domestically for more than 20 years, Robbins said. “The pipeline of Israeli technology companies migrating to the U.S. has provided a differentiated opportunity set,” he said, noting that Valley would continue to partner with Bank Leumi USA’s parent company on the VC front.

Bank Leumi Le-Israel has a more than 50% tech banking market share in Israel, he noted. “As part of our ongoing relationship, we will continue to benefit as the U.S. bank of choice for these Israeli referrals,” Robbins said.

Bank Leumi USA’s technology and VC banking teams currently serve more than 20 VC funds and 500 technology companies “and continue to establish additional relationships,” he said. “We believe there will be additional opportunities to expand this business in new markets going forward.”

Currently, the VC team contributes loan balances of only $60 million, but as tech companies mature, Robbins said Valley can grow that portion of the book.

“Opportunities exist to increase venture and asset-based lending on a combined basis,” he said. “The tailwinds for growth in this area are significant.”

The deal would also expand Valley’s commercial-and-industrial book, provide it a new venture capital line of business, boost fee income and reduce its deposit costs, according to Michael Hagedorn, Valley’s chief financial officer.

“These are very compelling reasons to do this deal,” Hagedorn said in an interview Thursday.

The acquisition is part of an ongoing effort to diversify Valley’s revenue streams and funding sources. Bank Leumi USA had total assets of $8.4 billion, total deposits of $7.1 billion, and gross loans of $5.4 billion as of June 30.

Together with Valley’s recently announced acquisition of Westchester Bank Holding Corp., which is expected to close in the fourth quarter, the Bank Leumi deal would bring Valley to $51 billion of assets, $42 billion of deposits and $39 billion of loans.

Valley, which currently operates in New Jersey and New York, agreed in June to acquire Westchester in White Plains, New York, for $220 million. Valley noted that deal would give it additional commercial lending expertise in the affluent Westchester County market.

The latest transaction, expected to close by the late first quarter or early second quarter of 2022, would be Valley’s 10th bank acquisition since 2008.

Hagedorn said the target’s C&I and commercial real estate lending operations complement Valley’s. The goal is to put more of Bank Leumi USA’s deposits into C&I loans as the economy grows and the combined bank capitalizes on its scale to compete nationally with the country’s biggest banks, he said. Valley would become a top 50 bank by assets after the deal closes in 2023.

Valley has aimed for loan growth at around 7%. Robbins told analysts that target stands, though post-acquisition, it could increase. “We definitely anticipate a much more diversified, stronger growth model as we continue to move the organization forward,” he said.

Hagedorn also noted that about 20% of Bank Leumi USA’s revenue comes from noninterest products. This trait would increase Valley’s revenue diversity, he said.

Bank Leumi’s fee income is primarily driven by cash management services for commercial customers, and investment management fees within its private bank. Fee income currently accounts for about 13% of Valley’s revenue, he said, but the company targets 20%.

The transaction is expected to be about 7% accretive to Valley’s 2023 earnings, assuming cost savings of 32.5%. Valley estimated tangible book value dilution at 1% with an earn-back period of one year.

Credit: Source link

Comments are closed.